Are you concerned about how QR code payments impact your PCI DSS compliance? Handling sensitive cardholder data through visual codes introduces specific security risks that can lead to significant fines or data breaches if not managed properly. This guide provides actionable steps to implement secure QR workflows that meet compliance standards and protect your revenue.

Understanding QR Codes and PCI DSS 4.0

The PCI DSS 4.0 standard, which becomes fully effective in March 2025, applies to any system that stores, processes, or transmits cardholder data. When you integrate QR codes into your checkout process, your compliance scope is determined by how that data flows through your environment. In a merchant-presented flow, you display a code that the customer scans with their smartphone. This often places your systems in scope because the transmission path typically involves your point-of-sale hardware or local network.

Alternatively, consumer-presented modes allow the customer to display a code from their mobile wallet for you to scan. This method often utilizes tokenized data, which can significantly reduce your compliance burden because the actual primary account numbers never touch your hardware. Understanding the ultimate guide to QR codes for mobile wallets can help you decide which architecture best fits your business needs while minimizing risk.

Security Vulnerabilities in the QR Payment Lifecycle

Before securing your system, you must recognize the vulnerabilities unique to QR technology. Unlike encrypted card swipes, physical QR codes are susceptible to tampering and quishing, a form of QR-based phishing. Attackers may place a fraudulent sticker over your legitimate code to redirect payments to their own accounts. For example, a major parking meter scam in San Francisco in 2024 resulted in over $100,000 in losses due to these types of tampered codes.

Digital threats are equally dangerous, as malicious redirects can lead users to cloned payment portals designed to harvest credentials. If a QR code transmits data over unencrypted channels, man-in-the-middle attacks can compromise the entire transaction. You can learn more about mitigating QR code payment risks to ensure your customers are not sent to counterfeit sites or exposed to malware.

Strategies to Reduce Your Compliance Scope

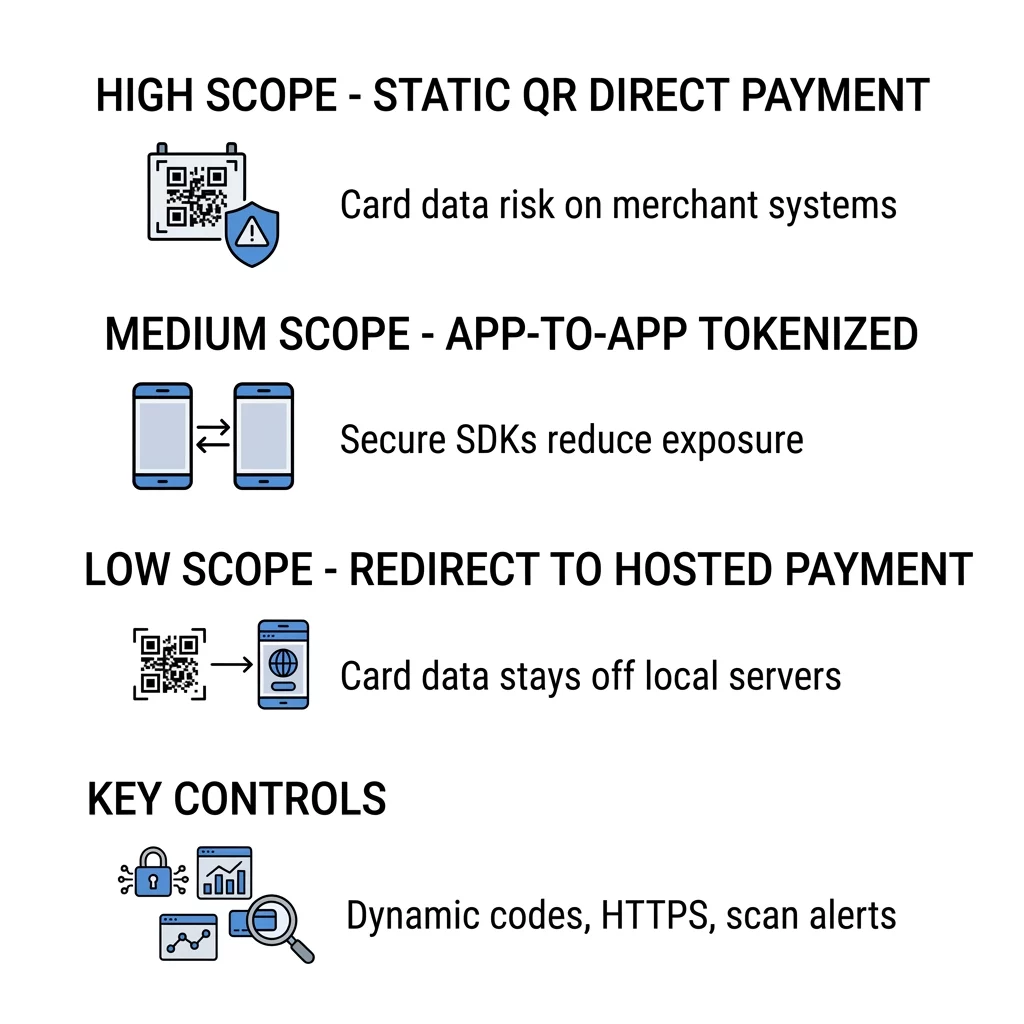

Your choice of payment architecture determines how much of your network is subject to rigorous annual audits. A redirect-to-hosted architecture is often the most efficient way to reduce scope. By using a link QR code generator to send customers directly to a PCI-validated payment service provider like Stripe or PayPal, you ensure that cardholder data never touches your local servers.

Other architectures involve varying levels of responsibility. While static codes used for direct payments carry a high scope and are generally not recommended for sensitive transactions, app-to-app integrations offer a middle ground by using secure SDKs and tokenization. Choosing a low-scope setup saves significant time and reduces the technical overhead required for maintaining your compliance certification.

Best Practices for Secure Implementation

Maintaining a compliant environment requires a combination of robust technical controls and active monitoring. Prioritizing dynamic codes over static ones is a fundamental security step. Unlike fixed patterns, static vs dynamic QR codes differ in their ability to be edited or deactivated. If you detect fraud on a dynamic code, you can update the destination URL or kill the link instantly without reprinting your physical signage.

Encryption is another non-negotiable requirement. You should ensure all payment-related codes utilize encryption to secure data, typically using AES-256 standards to protect the payload. Additionally, you should monitor your analytics for scan anomalies. If a QR code meant for a local storefront is suddenly receiving scans from international IP addresses, your system should be configured to flag this activity for investigation immediately.

Secure Your Payment Workflow Use the Pageloot QR code generator to create branded, dynamic codes with advanced security features and real-time tracking. Start Your Free 14-Day Trial

Operational Security and Staff Oversight

Compliance extends beyond software to include human behavior and physical maintenance. Your staff serves as the first line of defense against physical tampering. You should train your team to perform daily visual inspections of all QR payment points, looking for misaligned stickers, changes in texture, or signs of an overlay.

Furthermore, ensure that your QR code placements follow QR code payment accessibility standards. Mounting codes between 15 and 48 inches off the ground ensures they are reachable for all customers, including wheelchair users, while making them easier for staff to monitor. Reviewing how QR code payments improve security and speed can help you find the right balance between a fast customer experience and strict data protection protocols.

Frequently Asked Questions

Yes, if the QR code is part of a workflow that transmits or processes cardholder data, it is considered in scope. However, you can significantly reduce the number of controls you must manage by using a redirect to a hosted payment page or by implementing tokenized mobile wallet payments.

Requirement 10 focuses on logging and monitoring access to network resources and cardholder data. Dynamic QR codes allow you to track every scan event, including timestamps, IP addresses, and device types, providing the necessary audit trail to detect and investigate unauthorized access attempts.

Most free generators lack essential security features like SSL encryption, password protection, and the ability to edit or revoke a destination URL. For payment processing, it is vital to use a professional platform that adheres to secure QR code generation best practices to prevent quishing and data interception.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}