Are you trying to assess where QR code payments are headed in developing markets? The answer shapes investment strategy, product decisions, and market-entry timing. This article breaks down the adoption drivers, regulatory frameworks, and growth forecasts you need to make sense of this fast-moving space.

Why Emerging Economies Are Leading QR Payment Adoption

QR code payments have grown faster in emerging markets than in developed ones – and the reasons are structural, not coincidental.

In many developing economies, traditional banking infrastructure is thin. Point-of-sale terminals are expensive, card networks have limited reach, and large portions of the population remain unbanked. QR codes solve several of these problems at once. A merchant needs only a printed code or a smartphone screen to accept digital payments – no card reader, no expensive hardware, no complex onboarding.

QR code payments are seen as a key tool for financial inclusion in emerging economies precisely because they allow small and micro-merchants to accept digital payments with minimal infrastructure, while connecting unbanked populations to formal financial services through mobile wallets. You can see how this plays out in practice through the QR code solutions available for banks and financial institutions.

China offers the clearest proof of concept. Research describes “massive adoption” of QR codes by merchants and consumers in day-to-day transactions, driven by affordable smartphones, wider mobile internet coverage, and a supportive digital ecosystem. The model has since been replicated and adapted across South and Southeast Asia, Latin America, and Sub-Saharan Africa.

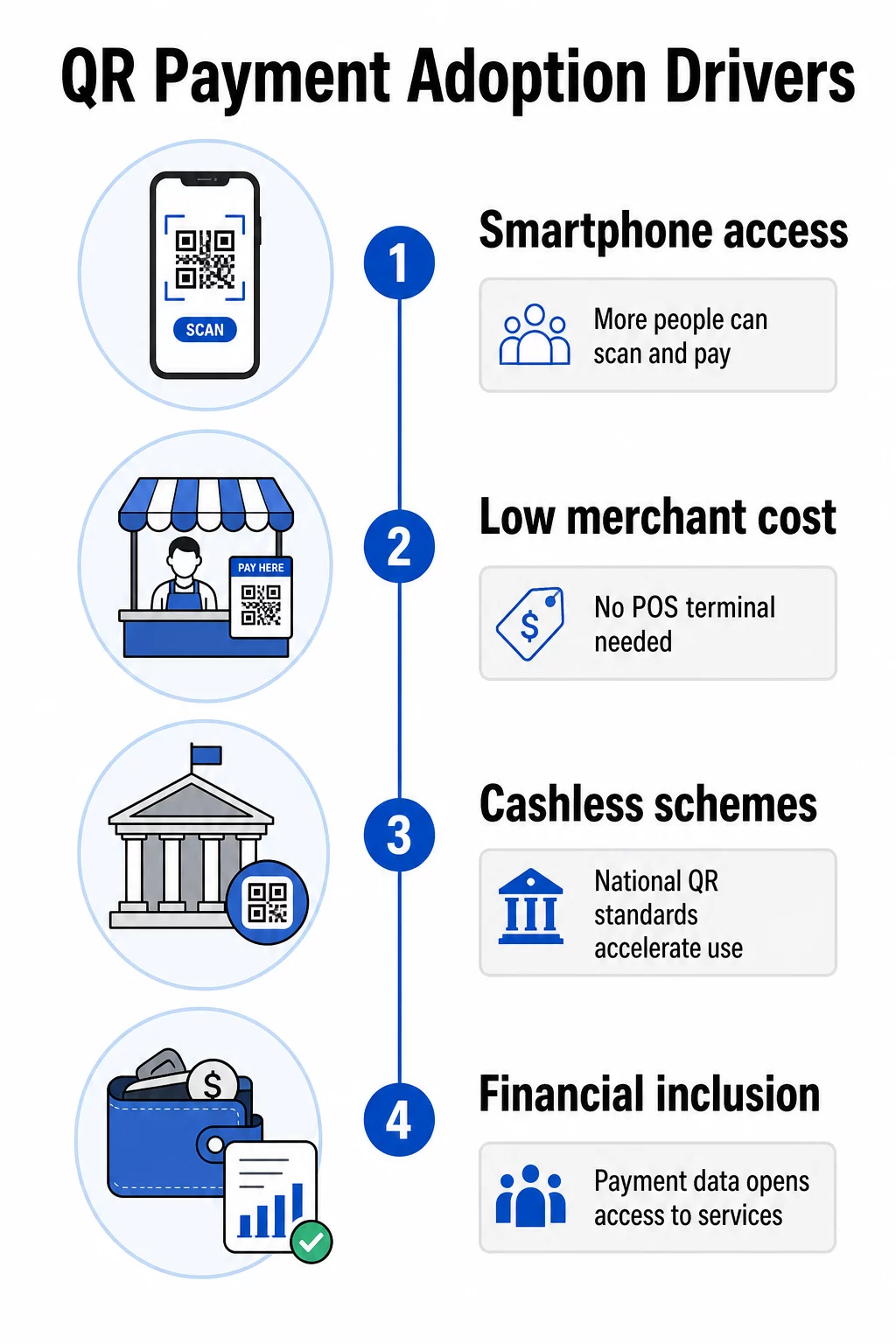

Key Drivers of QR Payment Adoption

Several distinct forces are accelerating QR payment uptake across emerging markets. These do not operate in isolation – they reinforce each other.

Smartphone penetration and ease of use

As smartphone costs fall, more consumers in low- and middle-income countries carry devices capable of scanning QR codes without a dedicated app. When paying requires nothing more than opening a camera app, the friction that typically slows payment technology adoption disappears.

Lower merchant costs

Compared to traditional POS terminals, QR-based acceptance has a dramatically lower cost of entry. For small traders operating on thin margins – street vendors, market stalls, small shops – this cost difference is decisive. 결제용 QR 코드 make it possible for any merchant to create and display a working payment code in minutes, without specialist equipment.

Government-backed cashless initiatives

National governments and central banks in several emerging economies have actively promoted QR payments as part of broader cashless policy agendas. India’s BharatQR, Indonesia’s QRIS, Sri Lanka’s LankaQR, Bangladesh’s Bangla QR, Ghana’s GhQR, Mexico’s CoDi, and Brazil’s Pix are all examples of state-backed systems designed to accelerate adoption at scale – particularly among informal sector merchants and low-income consumers.

Financial inclusion as a policy goal

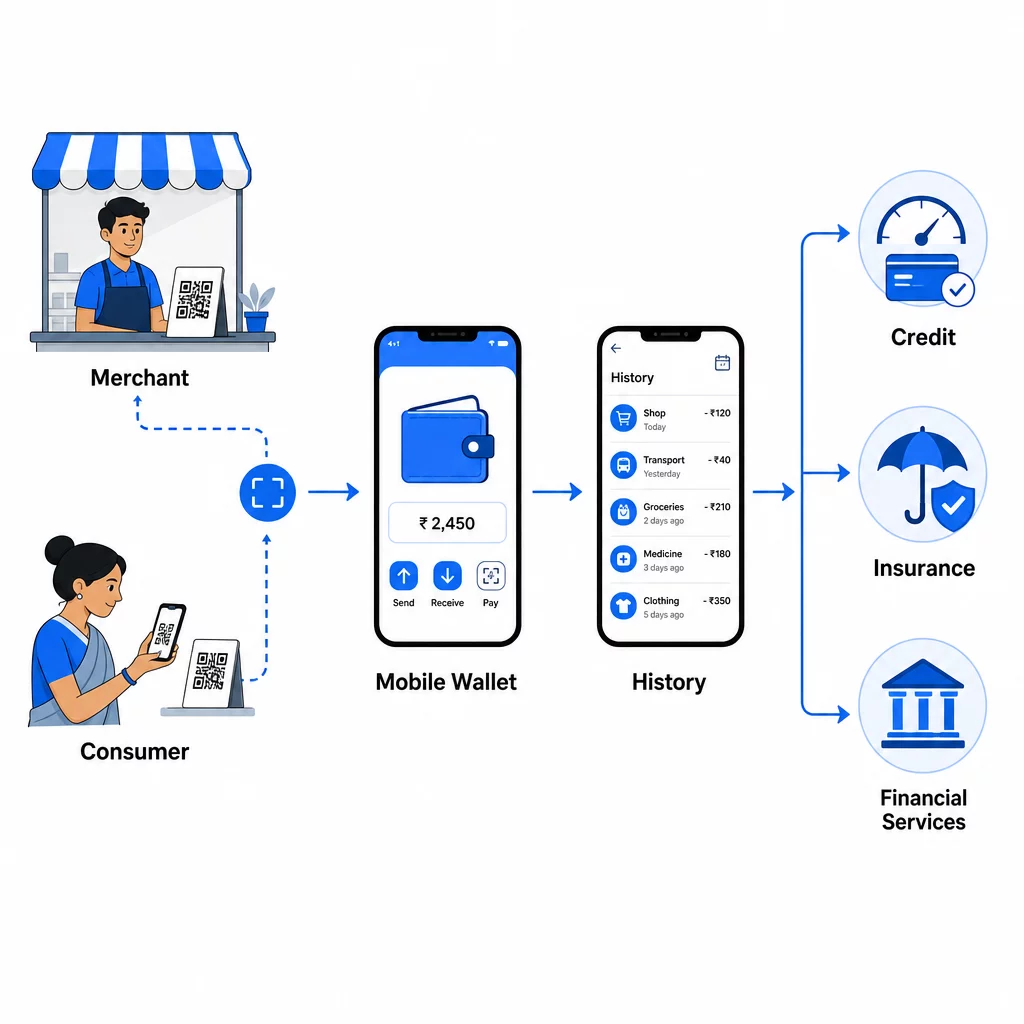

Beyond convenience, QR payments create something valuable over time: a transaction history. For previously unbanked individuals and merchants, this data trail can eventually unlock access to credit, insurance, and other formal financial services. As CGAP notes, easy and widespread digital payment opportunities “can bring lasting and profound behavior change among low-income customers and merchants, making formal payments a part of their everyday lives.”

Mobile wallet growth and digital ecosystems

The rise of mobile wallets – Alipay and WeChat Pay in China, Paytm in India, GoPay and OVO in Indonesia, M-Pesa derivatives across Africa – has created ready-made user bases for QR payments. Understanding how Alipay and WeChat Pay QR code integration works in practice gives you a useful reference point for how mature QR payment ecosystems function.

Social influence and trust

Research on QR payment adoption in Cambodia identified trust, service quality, social influence, and perceived risk as significant user-level drivers. In markets where cash remains culturally dominant, visible peer adoption and institutional credibility carry more weight than in markets where digital payments are already the norm.

Market Size and Growth Forecasts

The numbers behind QR payment growth are substantial enough to demand serious attention from investors and strategists.

- The global QR code payment market was estimated at approximately USD 12.5 billion in 2024 and is projected to reach USD 61.7 billion by 2033, representing a compound annual growth rate of around 20%.

- A separate forecast projects that total QR code payment spend will rise from USD 5.4 trillion in 2025 to USD 8 trillion in 2029 – a 48% increase over four years.

- An earlier projection estimated growth from USD 8.07 billion in 2020 to USD 35.07 billion by 2030 at a 16.1% CAGR.

Asia-Pacific, which contains many of the world’s largest emerging economies, is expected to hold the largest share of global growth throughout the forecast period. China, India, and Southeast Asian nations are the primary contributors, supported by both market-driven mobile wallet expansion and deliberate government cashless initiatives.

While these figures are global rather than emerging-market-specific, the underlying drivers are concentrated in developing economies. Growth in mature markets like the United States has been comparatively slower. As more merchants adopt QR code payment options to make transactions faster, safer, and more accessible, that concentration is likely to deepen.

The Regulatory Landscape: Standards, Interoperability, and Oversight

Regulation in this space is not a barrier so much as an architecture. How central banks and governments structure QR payment schemes shapes who can participate, how costs are distributed, and how fast adoption can scale.

National QR standards and interoperability

The most significant regulatory development in emerging economies is the proliferation of interoperable national QR standards. These schemes – developed and often owned by central banks or national payment authorities – use EMVCo standards to ensure that a single QR code can accept payments from multiple providers. This matters enormously for merchant adoption: a small trader who accepts one QR scheme effectively accepts all participating wallets and banks.

| 국가 | Scheme | Operator |

|---|---|---|

| India | BharatQR | Reserve Bank of India / NPCI |

| Indonesia | QRIS | Bank Indonesia |

| Sri Lanka | LankaQR | Central Bank of Sri Lanka |

| Bangladesh | Bangla QR | Bangladesh Bank |

| Ghana | GhQR | Ghana Interbank Payment and Settlement Systems |

| Mexico | CoDi | Banco de México |

| Brazil | Pix | Banco Central do Brasil |

| Kyrgyzstan | ELQR | National Payment System |

LankaQR, introduced in 2018, is explicitly required to comply with global EMV standards – a design choice that enables any bank or payment provider to accept payments through a unified code, without proprietary lock-in.

Cross-border interoperability

The ASEAN Integrated QR Code Payment System links national QR schemes across participating countries under the ASEAN Local Currency Transaction Framework. This policy initiative supports cross-border QR payments in local currencies, reducing dependence on foreign currency intermediaries for regional transactions. For businesses and investors with a regional rather than single-country focus, this integration significantly expands the addressable market.

Consumer protection and privacy

The OECD recommends that digital financial literacy initiatives run alongside financial consumer protection frameworks. In practice, regulations around QR payments should not only mandate technical security standards but also ensure consumers have access to transparent information and effective mechanisms to report fraud. For businesses operating across multiple jurisdictions, understanding how QR code privacy laws and key regulations apply to payment data is an important compliance consideration.

This is increasingly relevant because QR payment growth has produced new fraud patterns in some countries. Static merchant QR codes are particularly vulnerable to physical replacement attacks – where a fraudster places a fake code over a legitimate one. The guide on QR code risks in payments and how to mitigate them covers the main threat vectors businesses face.

The limits of available regulatory data

Public sources provide high-level descriptions of central bank roles and EMV standards, but granular, country-by-country statutory provisions specifically governing QR code payments are not well documented. Investors and strategists conducting due diligence in specific markets will need to supplement these frameworks with local legal analysis.

Financial Inclusion: The Long-Term Strategic Case

For investors and development-focused strategists, the financial inclusion dimension of QR payments is arguably the most consequential long-term trend.

QR codes create a low-cost entry point into the formal digital economy for two groups who have historically been excluded: small merchants and low-income consumers. As QR adoption spreads in these segments, it generates transaction histories that can serve as alternative credit data. Over time, this data trail creates pathways to credit, insurance, and other financial services – products that represent substantial addressable markets in their own right.

CGAP frames this clearly: QR codes are “a promising way to digitize payments at low-income merchants and get customers to go digital,” and the transaction histories they generate “can bring access to credit and other formal financial services, creating a gateway to financial inclusion.”

Experience from East Asia reinforces this point. As QR-based mobile payments substitute for cash, banks can reduce costs associated with cash services – freeing capital for lending and other value-adding activities. The financial inclusion case is not purely theoretical; it is backed by observable behavior change at scale.

Risks and Barriers to Watch

The growth case is strong, but no honest market analysis ignores the headwinds.

Fraud and security vulnerabilities

Static QR codes can be physically tampered with, and the inability of most users to verify a code’s destination before scanning creates ongoing fraud risk. As adoption scales, fraud patterns tend to scale with it. The security and speed advantages of QR code payments are real, but they depend on implementation choices – particularly the use of dynamic codes over static ones – not the technology alone.

Trust and digital literacy gaps

Research from Cambodia and other emerging market contexts consistently identifies trust as a primary adoption barrier. Where consumers lack confidence in digital systems – or where prior fraud experiences have damaged trust – adoption stalls regardless of infrastructure quality. Government-backed digital literacy initiatives are part of the policy response, but progress is uneven.

Fragmentation risks

While interoperable national standards reduce fragmentation within countries, cross-border interoperability remains incomplete. Businesses operating across multiple emerging markets face the practical challenge of navigating different schemes, standards, and regulatory environments. The ASEAN integration effort is a meaningful step forward, but it covers a limited set of countries.

Infrastructure dependencies

QR payments require reliable mobile internet connectivity. In rural areas and lower-income urban zones – precisely the populations most relevant to financial inclusion goals – connectivity can be inconsistent. This constraint limits how quickly QR adoption can reach the most underserved segments.

What This Means for Businesses Operating in These Markets

For companies already accepting or planning to accept QR code payments across emerging economies, a few practical considerations follow from this analysis.

- Design payment acceptance around the dominant local scheme. Merchant acceptance of QRIS in Indonesia or UPI-linked QR in India reaches a far wider customer base than accepting only one proprietary wallet. Interoperable standards exist precisely to eliminate that kind of lock-in.

- Use dynamic QR codes rather than static ones. Dynamic codes let you update payment destinations, monitor scan activity for anomalies, and deactivate codes if fraud is detected – all without reprinting. For businesses managing payments across multiple locations, this centralized control is operationally significant. The guide to QR codes for mobile wallets explains the practical differences between dynamic and static approaches in a payment context.

- Treat analytics as a core function, not an afterthought. Understanding when and where codes are being scanned – and flagging unusual patterns – is as relevant to fraud prevention as it is to marketing optimization. Businesses that use QR codes for peer payments effectively tend to monitor scan data actively rather than reactively.

- Build for the interoperable future. Cross-border QR payment integration is expanding. Businesses that invest now in flexible, scheme-agnostic acceptance infrastructure are better positioned to scale as regional frameworks like the ASEAN system mature.

Start Accepting QR Payments Without the Complexity Need to create payment QR codes that work across your business locations? Use the Pageloot QR 코드 생성기 to build dynamic, trackable codes – or the PayPal QR 코드 생성기 to link directly to your payment account with no hardware required.

The Trajectory Is Clear, the Details Are Still Being Written

QR code payments in emerging economies are not a speculative trend – they are an infrastructure reality backed by central bank mandates, demonstrated adoption at scale, and a growth rate that outpaces most segments of the payments industry. The market is projected to grow at roughly 20% annually through 2033, with Asia-Pacific leading and Latin America, Africa, and South Asia contributing meaningfully.

The strategic question for investors and business leaders is not whether QR payments will dominate digital commerce in emerging economies, but how quickly fraud governance, cross-border interoperability, and digital literacy will mature to support that dominance. Those who understand the regulatory architecture – and position themselves within the interoperable national standards that central banks are actively promoting – are best placed to capture the opportunity.

For businesses building QR payment capabilities today, explore the QR code solutions available across industries to find the right approach for your sector.

자주 묻는 질문

Emerging markets have less existing card payment infrastructure, higher proportions of unbanked populations, and lower smartphone costs relative to POS terminal costs. QR codes remove the need for expensive hardware, allowing any merchant with a printed code or smartphone to accept digital payments. Government-backed cashless initiatives and interoperable national QR standards have also accelerated adoption in ways that have no direct equivalent in most developed markets.

Central banks in many emerging economies have taken a direct role in developing and mandating interoperable national QR schemes – examples include BharatQR in India, QRIS in Indonesia, LankaQR in Sri Lanka, and Pix in Brazil. These schemes use EMVCo standards to ensure that a single QR code can accept payments from multiple providers, reducing fragmentation and supporting adoption among small merchants and low-income consumers. This is a policy-driven infrastructure investment, not simply a market outcome.

The most common risks are physical QR code tampering (where fraudsters replace a legitimate code with a fake one redirecting payments to their own account) and phishing attacks that mimic legitimate payment pages. Using dynamic QR codes – which can be monitored for unusual scan activity and deactivated if compromised – significantly reduces these risks compared to static codes. For a full breakdown of threats and mitigation strategies, see the guide on QR code risks in payments.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}