Are your customers still struggling with clunky authentication flows, slow loan paperwork, and card-dependent payments? These friction points cost banks customers and erode trust. This guide explains exactly how QR codes can streamline those experiences – from mobile payments and cardless ATM access to in-branch identity verification.

How QR Code Payments Are Reshaping Banking Globally

QR-based payments are no longer a regional curiosity. Countries across Asia, South America, and Africa have built national-scale QR payment infrastructure, and U.S. financial institutions are increasingly catching up.

In China, platforms like Alipay and WeChat Pay turned QR payments into the default transaction method across all income levels. India’s BharatQR system became the world’s first interoperable payment acceptance solution, standardizing QR acceptance across banks and processors. Platforms like Alipay and WeChat Pay allow customers to pay by scanning QR codes, offering a fast, cashless transaction method that works for merchants of any size.

In the U.S., major payment platforms including PayPal, Venmo, and Square have embedded QR payment flows into their products. U.S. banks use QR codes to let customers manage investments, pay bills, access accounts, and transfer money – all from a smartphone. The payment details transmit securely between customer and institution via end-to-end encryption verified by the bank.

For financial institutions evaluating adoption, understanding how QR code payments work for businesses is a practical first step.

Key Use Cases for QR Codes in Banking and Finance

Mobile and Contactless Payments

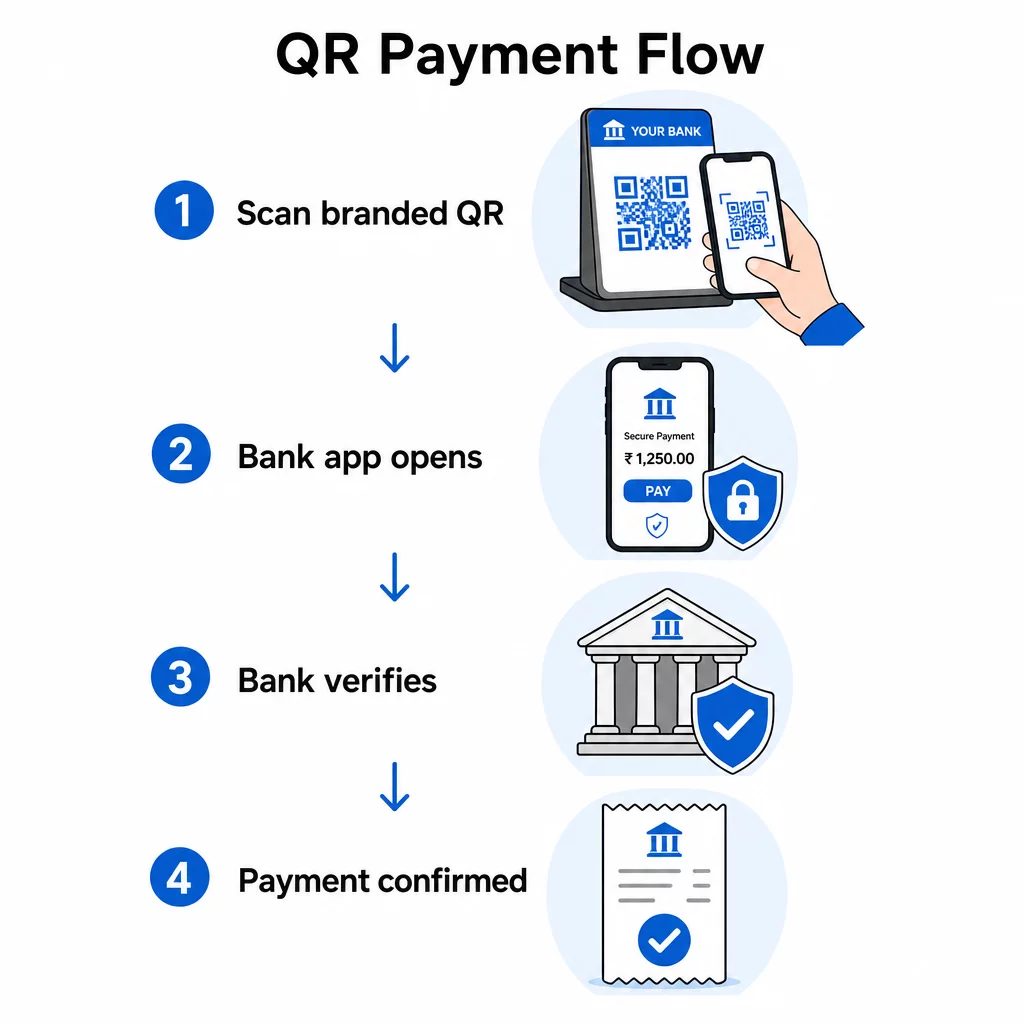

UNA payment QR code is a scannable code that allows customers to complete financial transactions using only their smartphones. The typical flow is simple: the customer scans the code, lands on a checkout page or payment app, enters payment details, and completes the transaction.

QR payment systems support a wide range of methods:

- Mobile wallets and bank apps

- PayPal, Venmo, and similar QR-based platforms

- Cryptocurrency wallets

- Contactless card-linked flows

- Retailer apps and loyalty-integrated payments

Banks can place QR codes at POS terminals, on invoices, in mobile banking apps, or in email and print correspondence. Customers don’t need a physical card – just the app and a camera.

Create QR Codes for Financial Services Looking to deploy QR codes across payment touchpoints or branch materials? Explore the QR Code Generator for Finance para empezar.

Cardless ATM Access and Authentication

Some U.S. banks have introduced cardless ATM workflows powered by QR codes. A customer opens their mobile banking app, which generates a QR code that they scan at the ATM’s barcode reader. The ATM authenticates the user and approves the transaction without requiring a physical card or PIN entry.

This reduces ATM skimming risk significantly, since no card data is ever exposed at the machine. It also benefits customers who forget their card or prefer not to carry one.

Multifactor Authentication and Account Security

Financial institutions incorporate QR codes into multifactor authentication (MFA) workflows. Rather than relying solely on a one-time password sent via SMS – a method vulnerable to SIM-swapping attacks – banks can use a time-limited QR code as an additional verification layer for login, wire transfers, or high-value transactions.

MFA using QR codes creates a more user-friendly experience while improving security. Customers scan the code with their authenticated banking app, which confirms their identity before the transaction proceeds.

In-Branch Identity Verification

Credit unions and community banks use QR codes to streamline in-branch identity verification. A member arrives at a branch, scans a QR code displayed at the counter, selects their institution, enters their member details, uploads an ID document, and takes a selfie – all on their own phone. A one-time passcode is then shown to the teller to complete the verification.

This approach reduces the time tellers spend handling documents and creates a clean, auditable digital record of each verification event.

Faster Loan Applications

QR codes reduce friction in multi-step processes like loan applications. Banks can generate a QR code that gives applicants direct access to:

- Required documents and checklists

- Online application forms

- Application status tracking

Applicants scan once and have everything they need in one place. Banks receive structured submissions instead of fragmented paperwork. The result is faster processing on both sides and a higher completion rate for applications.

Instant Account Statements and Verification

Banks can generate customer-specific QR codes that provide instant, authenticated access to account statements. Use cases include:

- Proof of net worth for lenders or landlords

- Income verification for third parties

- Personal financial tracking

Password-protecting these QR codes adds an additional layer of access control, so the statement can only be viewed by someone with the right credentials.

Static vs. Dynamic QR Codes: What Banks Need to Know

Not all QR codes work the same way in financial contexts. The distinction between códigos QR estáticos y dinámicos has direct consequences for security, compliance, and operational flexibility.

| Característica | Código QR estático | Código QR dinámico |

|---|---|---|

| Editable después de la creación | No | Sí |

| Análisis de escaneos | Ninguno | Real-time tracking |

| Can be deactivated | No | Sí |

| Per-transaction unique codes | No | Sí |

| Tamper recovery | Requires reprinting | Update destination instantly |

Dynamic QR codes are strongly preferred for financial services. They can be generated per transaction, expire automatically, be bank-verified in real time, and deactivated immediately if fraud is detected. Static codes, by contrast, are fixed – if one is compromised or tampered with, it cannot be updated without reprinting.

For ongoing campaigns, account access codes, and anything tied to financial transactions, tracking QR code performance with dynamic codes also allows institutions to monitor scan patterns and detect anomalies before they escalate.

Security Considerations and Risk Controls

QR codes used for payments or account access do not provide built-in security. The application, banking platform, or payment processor must enforce encryption, authentication, and fraud controls. Understanding the risks is the first step to mitigating them.

Quishing (QR phishing) is one of the most common threats. Malicious codes redirect users to fake banking portals that capture login credentials or payment data. These sites can look identical to official banking pages.

Physical tampering is also a documented risk. Fraudsters place sticker overlays on legitimate QR codes – whether on branch materials, invoices, or POS terminals – redirecting payments to attacker-controlled accounts. In one documented case, police in Austin, Texas discovered 29 fake QR codes placed on city parking meters.

Banks and financial institutions can reduce these risks by following established mejores prácticas para la generación segura de códigos QR:

- Use dynamic QR codes that can be deactivated and updated instantly

- Brand all QR codes with institutional logos and colors to make tampering visible

- Conduct regular physical inspections of QR codes placed in branches and at ATMs

- Configure code expiration for transaction-specific flows

- Monitor scan analytics for unusual geographic patterns or spike activity

For institutions accepting QR payments, PCI-DSS compliance is required. This means securing QR generation infrastructure, using TLS for data transmission, and never storing sensitive post-authorization data. Businesses redirecting to third-party processors may qualify for the simplified SAQ A compliance path.

A detailed breakdown of the risks specific to payment QR flows – including phishing, data interception, and malware distribution – is covered in the guide on QR code risks in payments and how to mitigate them.

For customers, recommended safe practices include verifying the code source, checking for signs of physical tampering, avoiding entering sensitive banking data after scanning an unfamiliar code, and manually typing known banking URLs when in doubt.

Compliance and Privacy Considerations

Beyond PCI-DSS, financial institutions operating internationally or serving customers across jurisdictions must account for data privacy regulations that apply to QR code scans. Each scan can collect IP address, device type, location, and behavioral data – all of which may be regulated under GDPR, CCPA, or other frameworks depending on where customers are located.

A full overview of applicable regulations and compliance tools is available in the QR code privacy laws and key regulations guide.

Dynamic QR codes help with compliance by enabling institutions to update privacy disclosures without reprinting codes, configure data retention, and maintain audit trails – all useful during regulatory assessments.

Monitoring QR Code Performance in Financial Contexts

One underused advantage of QR codes in financial services is the analytics layer that dynamic codes provide. A QR code management platform can capture:

- Number of scans per code and per location

- Time and date of each scan

- Geographic distribution of scan activity

- Device type and operating system

For banks, this data supports several operational goals. Unusual scan patterns – such as a branch payment code suddenly generating scans from unexpected international locations – can trigger alerts and prompt a security review. Aggregate data on loan application QR engagement can show where applicants are dropping off. Branch visit QR codes reveal which locations see the most digital engagement.

Track QR Code Performance Across Your Institution Utilice dynamic QR codes with built-in analytics to monitor scan activity, detect anomalies, and understand how customers engage with your digital touchpoints.

Getting Started with QR Codes for Your Financial Institution

QR codes work across nearly every customer touchpoint a bank operates: branch desks, ATM vestibules, printed statements, email communications, mobile banking apps, and digital signage. The technology requires minimal hardware investment since most customers already carry the only scanner they need – their smartphone.

For institutions starting out, the Generador de códigos QR de Pageloot supports both static and dynamic QR codes, with customization options for branding and a built-in analytics dashboard. For payment-specific implementations, the Generador de códigos QR de PayPal provides a straightforward path to QR-enabled payment acceptance.

The right starting point depends on your institution’s priorities – whether that is reducing authentication friction, speeding up loan intake, or enabling branch-level contactless payments. Each use case is achievable with the same underlying technology, and each one builds toward a more seamless, secure experience for your customers.

Preguntas Frecuentes

A static QR code stores fixed information that cannot be changed after creation and provides no scan analytics. A dynamic QR code uses a redirect URL that can be updated, deactivated, or replaced without reprinting. For banking use cases – especially payments and account access – dynamic codes are preferred because they can be generated per transaction, configured to expire, monitored for unusual activity, and disabled immediately if fraud is detected.

QR codes themselves are not inherently secure or insecure – security depends on the platform and controls built around them. Banks using QR codes for payments should enforce end-to-end encryption, use dynamic codes with per-transaction generation, require authentication through a verified banking app, and monitor scan analytics for anomalies. Institutions accepting QR payments must also comply with PCI-DSS requirements. Physical codes in branches and at ATMs should be inspected regularly for tampering.

In the U.S., financial institutions accepting QR code payments must comply with PCI-DSS, which governs the security of cardholder data across the payment lifecycle. Institutions serving international customers or operating across jurisdictions may also need to address GDPR, CCPA, or other regional privacy laws, depending on the data collected during QR interactions. Dynamic QR codes support compliance by enabling audit trails, data retention controls, and the ability to update privacy disclosures without reprinting.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}